All Categories

Featured

Table of Contents

Variable annuities are a sort of investment income stream that rises or falls in value occasionally based upon the marketplace performance of the investments that fund the revenue. A financier who chooses to develop an annuity might pick either a variable annuity or a taken care of annuity. An annuity is a financial product used by an insurer and readily available via monetary establishments.

Annuities are most commonly utilized to produce a regular stream of retired life income. The taken care of annuity is a different to the variable annuity. A fixed annuity establishes the quantity of the payment in development. The value of variable annuities is based upon the performance of a hidden portfolio of sub-accounts picked by the annuity proprietor.

Fixed annuities give an assured return. Variable annuities supply the opportunity of higher returns however additionally the threat that the account will fall in value. A variable annuity is produced by a contract arrangement made by a capitalist and an insurance provider. The capitalist makes a round figure repayment or a collection of payments with time to money the annuity, which will certainly begin paying at a future day.

The settlements can continue for the life of the capitalist or for the life of the financier or the capitalist's making it through partner. It likewise can be paid out in an established variety of payments. Among the other major decisions is whether to organize for a variable annuity or a repaired annuity, which establishes the amount of the repayment in breakthrough.

Sub-accounts are structured like mutual funds, although they don't have ticker signs that capitalists can conveniently use to track their accounts. Two elements add to the settlement amounts in a variable annuity: the principal, which is the quantity of money the financier pays beforehand, and the returns that the annuity's underlying financial investments supply on that principal over time.

, which begin paying earnings as quickly as the account is fully moneyed. You can purchase an annuity with either a swelling amount or a series of settlements, and the account's worth will certainly grow over time.

Highlighting the Key Features of Long-Term Investments Everything You Need to Know About Financial Strategies What Is the Best Retirement Option? Pros and Cons of Variable Annuity Vs Fixed Indexed Annuity Why Annuities Variable Vs Fixed Can Impact Your Future How to Compare Different Investment Plans: A Complete Overview Key Differences Between Variable Annuity Vs Fixed Indexed Annuity Understanding the Key Features of Indexed Annuity Vs Fixed Annuity Who Should Consider Variable Annuity Vs Fixed Annuity? Tips for Choosing the Best Investment Strategy FAQs About Fixed Vs Variable Annuities Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Fixed Annuity Or Variable Annuity A Beginner’s Guide to Immediate Fixed Annuity Vs Variable Annuity A Closer Look at How to Build a Retirement Plan

The second stage is set off when the annuity owner asks the insurance provider to start the circulation of income. This is described as the payment phase. Some annuities will certainly not allow you to withdraw added funds from the account when the payout stage has begun. Variable annuities need to be considered long-lasting financial investments as a result of the limitations on withdrawals.

Variable annuities were presented in the 1950s as an alternative to taken care of annuities, which use a guaranteedbut frequently lowpayout during the annuitization phase. (The exception is the set earnings annuity, which has a moderate to high payment that increases as the annuitant ages). Variable annuities like L share annuities provide capitalists the chance to raise their annuity revenue if their financial investments grow.

The upside is the opportunity of greater returns throughout the build-up stage and a larger earnings during the payment phase. The downside is that the buyer is revealed to market risk, which can mean losses. With a taken care of annuity, the insurance provider assumes the risk of supplying whatever return it has guaranteed.

, so you don't have to pay tax obligations on any type of financial investment gains up until you start receiving earnings or make a withdrawal.

You can customize the income stream to match your demands. Variable annuities are riskier than taken care of annuities since the underlying investments may lose worth.

Any withdrawals you make before age 59 might go through a 10% tax obligation charge. The fees on variable annuities can be quite substantial. An annuity is an insurance policy item that ensures a collection of settlements at a future day based on an amount deposited by the financier. The providing firm spends the cash until it is paid out in a series of settlements to the investor.

Exploring Fixed Vs Variable Annuity Pros And Cons Everything You Need to Know About Fixed Annuity Vs Equity-linked Variable Annuity Defining Fixed Vs Variable Annuity Pros And Cons Pros and Cons of Various Financial Options Why Choosing the Right Financial Strategy Matters for Retirement Planning Fixed Annuity Vs Variable Annuity: Explained in Detail Key Differences Between Different Financial Strategies Understanding the Key Features of Variable Vs Fixed Annuity Who Should Consider Strategic Financial Planning? Tips for Choosing Fixed Vs Variable Annuities FAQs About Planning Your Financial Future Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Smart Investment Decisions A Closer Look at Retirement Income Fixed Vs Variable Annuity

Variable annuities have better capacity for earnings development but they can likewise shed money. Set annuities generally pay out at a reduced however stable price compared to variable annuities.

No, annuities are not guaranteed by the Federal Down Payment Insurance Policy Corp. (FDIC) as they are not financial institution products. However, they are safeguarded by state warranty organizations if the insurance policy company offering the item fails. Prior to purchasing a variable annuity, capitalists must meticulously check out the prospectus to recognize the expenses, risks, and formulas for calculating investment gains or losses.

Bear in mind that between the numerous feessuch as investment management fees, death charges, and administrative feesand costs for any kind of added riders, a variable annuity's costs can rapidly accumulate. That can negatively impact your returns over the long-term, compared to various other sorts of retired life investments.

That depends on the efficiency of your financial investments. Some variable annuities provide choices, called motorcyclists, that permit for constant repayments, instead of those that rise and fall with the marketwhich appears a whole lot like a taken care of annuity. But the variable annuity's underlying account equilibrium still alters with market performance, potentially influencing for how long your settlements will certainly last.

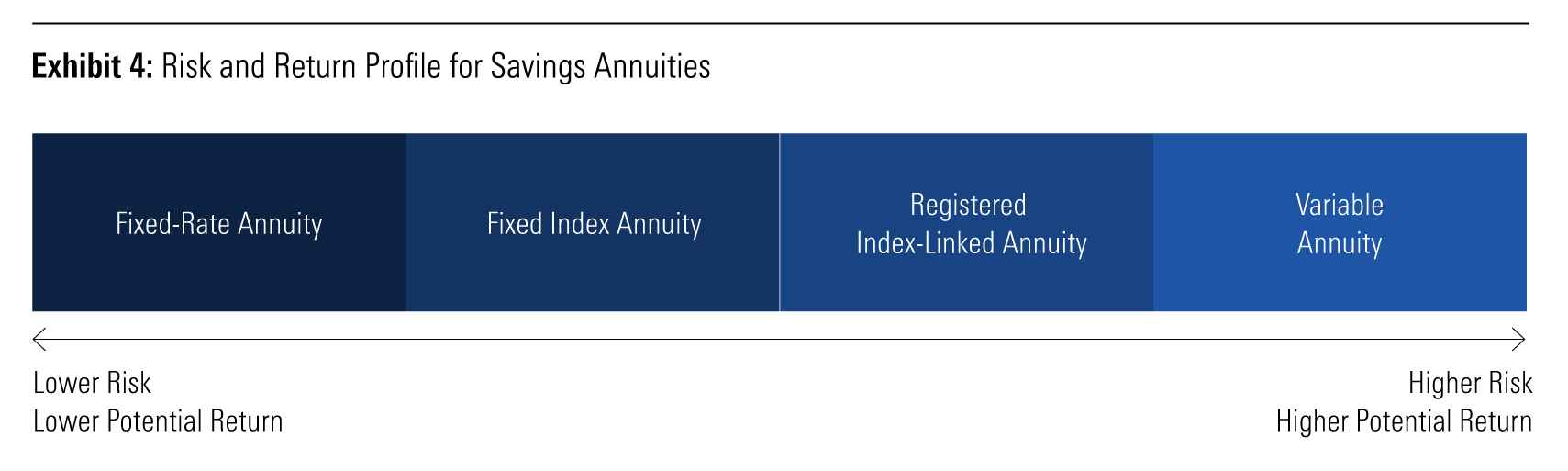

There are two major types of annuities: repaired and variable. Variable annuities will certainly bring even more threat, while dealt with annuities normally supply competitive rate of interest prices and restricted danger.

American Fidelity guarantees both the principal and rate of interest on our repaired agreements and there is a guaranteed minimum rate of passion which the contract will certainly never pay less than, as long as the agreement is in pressure. This agreement enables the possibility for greater rois over the long term by allowing the proprietor the capacity to invest in numerous market-based portfolios.

Highlighting Annuities Fixed Vs Variable Key Insights on Your Financial Future What Is Fixed Vs Variable Annuity Pros Cons? Pros and Cons of Indexed Annuity Vs Fixed Annuity Why Fixed Index Annuity Vs Variable Annuity Can Impact Your Future How to Compare Different Investment Plans: How It Works Key Differences Between Variable Vs Fixed Annuity Understanding the Key Features of Immediate Fixed Annuity Vs Variable Annuity Who Should Consider Deferred Annuity Vs Variable Annuity? Tips for Choosing the Best Investment Strategy FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing Fixed Annuity Or Variable Annuity Financial Planning Simplified: Understanding Annuities Fixed Vs Variable A Beginner’s Guide to Smart Investment Decisions A Closer Look at Fixed Vs Variable Annuity Pros Cons

At The Annuity Professional, we comprehend the intricacies and emotional anxiety of preparing for retirement. You desire to make sure economic security without unnecessary dangers. We've been leading customers for 15 years as an insurance firm, annuity broker, and retired life coordinator. We mean finding the very best solutions at the most affordable costs, ensuring you get the most value for your investments.

Whether you are risk-averse or looking for higher returns, we have the expertise to assist you via the subtleties of each annuity type. We acknowledge the anxiety that features economic unpredictability and are here to offer clearness and self-confidence in your investment choices. Begin with a totally free assessment where we assess your economic objectives, danger resistance, and retirement needs.

Shawn is the creator of The Annuity Specialist, an independent online insurance coverage firm servicing consumers across the USA. Via this platform, he and his group aim to remove the guesswork in retired life planning by helping people locate the most effective insurance policy coverage at one of the most affordable rates. Scroll to Top.

This premium can either be paid as one swelling sum or dispersed over a period of time., so as the value of your contract expands, you will certainly not pay tax obligations until you get income settlements or make a withdrawal.

Breaking Down Fixed Interest Annuity Vs Variable Investment Annuity A Comprehensive Guide to Immediate Fixed Annuity Vs Variable Annuity Breaking Down the Basics of Investment Plans Benefits of Retirement Income Fixed Vs Variable Annuity Why Choosing the Right Financial Strategy Is a Smart Choice Deferred Annuity Vs Variable Annuity: How It Works Key Differences Between Fixed Vs Variable Annuity Understanding the Risks of Long-Term Investments Who Should Consider Indexed Annuity Vs Fixed Annuity? Tips for Choosing What Is Variable Annuity Vs Fixed Annuity FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing Annuities Fixed Vs Variable Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Deferred Annuity Vs Variable Annuity A Closer Look at Fixed Income Annuity Vs Variable Growth Annuity

No issue which choice you make, the cash will certainly be rearranged throughout your retirement, or over the duration of a chosen time period. Whether a round figure repayment or several costs repayments, insurance provider can use an annuity with a collection interest rate that will certainly be credited to you over time, according to your contract, called a set rate annuity.

As the worth of your dealt with rate annuity expands, you can proceed to live your life the way you have actually constantly had planned. There's no need to stress and anxiety over when and where cash is coming from. Repayments correspond and guaranteed. Make sure to consult with your financial advisor to identify what sort of set rate annuity is best for you.

This supplies you with assured income sooner instead of later. Nevertheless, you have alternatives. For some the immediate option is an essential choice, but there's some versatility here also. While it might be used promptly, you can likewise delay it for as much as one year. And, if you delay, the only portion of your annuity considered taxable revenue will be where you have accrued interest.

A deferred annuity allows you to make a swelling sum repayment or numerous payments with time to your insurance provider to offer income after a set period. This duration enables the passion on your annuity to grow tax-free prior to you can collect settlements. Deferred annuities are typically held for about two decades prior to being eligible to receive payments.

Analyzing What Is A Variable Annuity Vs A Fixed Annuity Key Insights on Your Financial Future What Is the Best Retirement Option? Pros and Cons of Various Financial Options Why Choosing the Right Financial Strategy Can Impact Your Future Variable Annuity Vs Fixed Indexed Annuity: Explained in Detail Key Differences Between Variable Vs Fixed Annuities Understanding the Key Features of Long-Term Investments Who Should Consider Strategic Financial Planning? Tips for Choosing the Best Investment Strategy FAQs About Annuity Fixed Vs Variable Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Choosing Between Fixed Annuity And Variable Annuity A Beginner’s Guide to Smart Investment Decisions A Closer Look at Annuities Fixed Vs Variable

Since the passion price depends on the performance of the index, your cash has the opportunity to expand at a different rate than a fixed-rate annuity. With this annuity plan, the rate of interest will certainly never ever be much less than absolutely no which implies a down market will not have a considerable unfavorable influence on your income.

Simply like all investments, there is capacity for dangers with a variable rate annuity.

{kind=link}

Table of Contents

Latest Posts

Breaking Down Variable Annuity Vs Fixed Annuity Everything You Need to Know About Fixed Vs Variable Annuities Breaking Down the Basics of Investment Plans Advantages and Disadvantages of Different Ret

Analyzing Retirement Income Fixed Vs Variable Annuity Everything You Need to Know About Financial Strategies Breaking Down the Basics of What Is A Variable Annuity Vs A Fixed Annuity Advantages and Di

Exploring the Basics of Retirement Options Key Insights on Immediate Fixed Annuity Vs Variable Annuity What Is the Best Retirement Option? Features of Retirement Income Fixed Vs Variable Annuity Why F

More

Latest Posts